On the 10th of February, the Authorite des Marches Financiers (AMF), published a proposal on the minimum environmental criteria required for a financial product to be categorised as Article 9 or Article 8 under the European regulation SFDR (Sustainable Finance Disclosure Regulations).

The proposal is based on an informal consultation conducted with financial actors. The AMF noted that there was a gap between the expectations expressed by investors and the reality of the practices of the application of SFDR, which has fuelled greenwashing.

They propose to implement minimum criteria for these financial products where the definition of sustainable investment is more concrete while investing in activities aligned to the EU Taxonomy.

Background of Article 9 and Article 8, under the SFDR

Adopted in 2019, the SDFR was framed by the European co-legislators and the Commission as an ESG transparency regime for financial entities and products.

As it written, the SFDR label asked financial actors to publish information about their sustainability claims and practices. Therefore, the current Art. 9 and Art. 8 classifications did not have an assessment for sustainability for the financial products and their investments. Consequently, the notion of “sustainable investment” is vague, and has given rise to different interpretations of what sustainability is.

To add tangibility, the AMF has developed a proposal for the minimum expectation of criteria for a financial product to be categorised as Art. 9 and Art. 8 under SFDR.

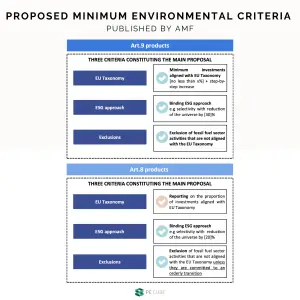

Summary of the Proposition

- The Commission should propose minimum criteria that a product would have to meet to be classified as Art. 9 and Art. 8 and should be subject to national supervision.

- The Article 2(17) of the SFDR should be replaced to include a concrete definition of sustainable investment

- A minimum proportion of the underlying assets in the Art. 9’s products should consist of investments in activities that are aligned with the EU Taxonomy.

- When making investment decisions on the underlying assets of Art. 9 and Art. 8 products, manufactures should be required to adopt an ESG binding approach

- Investments in the fossil fuel sector that are not aligned with the EU Taxonomy, should be excluded from Art. 9 products. As for Art. 8, investments in such activities are permitted as long as certain criteria are met to ensure that they are dedicated to an orderly transition.

Additional requirements for the future minimum standards:

- The adoption and disclosure of engagement policies at the level of such products may be required by manufacturers of Art. 9 and Art. 8 products.

- Manufacturers of Art.9 and Art.8 products could be required to report on the principal adverse impacts (PAI) of their investment decisions in relation to these specific products.

- Investments in “transition assets” could make up a minimum proportion of Art.9 and Art.8 products’ underlying assets.

Read the full version of the proposal on the AMF website.

Consequences

As the AMF becomes more stringent in the definition of sustainable investments and a minimum environmental criterion is defined, it is crucial for fund managers to be able to track ESG and non-financial metrics when tracking your portfolio companies.

Book a démo, to learn how PE Cube can accompany you to follow the pertinent portfolio metrics, all while allowing fund managers to track ESG and non-financial metrics.